Radiopharmaceuticals heat up: China's new players join the global fray

In the field of radiopharmaceuticals, Pluvicto has undoubtedly become the most discussed topic this year.

As a blockbuster radiopharmaceutical product from Novartis, Pluvicto achieved USD 1.392 billion in sales in 2024, representing a year-on-year growth of 42%, establishing its blockbuster status. In the first three quarters of this year, Pluvicto's revenue reached USD 1.389 billion, nearly matching the full-year sales of the previous year, with a year-on-year growth of 33%. At the JPM 2025 Conference, Novartis projected Pluvicto's peak sales to exceed USD 5 billion.

Another Novartis radiopharmaceutical product, Lutathera, achieved sales of USD 724 million last year, approaching the billion-dollar threshold.

Among Chinese companies, Grand Pharma entered the radiopharmaceutical field by acquiring Australia's Sirtex and introducing Yttrium-90 [90Y] Microsphere Injection. This product was approved for marketing in China in 2022 for the treatment of colorectal cancer liver metastases. Since its approval in China, Yttrium-90 [90Y] Microsphere Injection has rapidly gained market traction, generating nearly HKD 500 million in revenue in 2024, a significant year-on-year increase of nearly 140%. In July 2025, the product received FDA approval for a new hepatocellular carcinoma (HCC) indication, paving the way for expansion into new markets.

The commercial success of radiopharmaceuticals has attracted more innovative pharmaceutical companies to this field. Beyond Novartis, multinational corporations (MNCs) such as Eli Lilly, Bristol Myers Squibb (BMS), AstraZeneca, and Roche are actively developing therapeutic radiopharmaceuticals.

Recent activities among Chinese innovative biopharma companies have also been frequent. Hengrui Pharma has established a radiopharmaceutical research platform in Tianjin and taken a leading role in forming the Tianjin Radiopharmaceutical Innovation Consortium. Kelun-Biotech has also entered radiopharmaceutical R&D; its core product, SKB107, has entered Phase I clinical trials, with the first patient dosed on August 15 this year, primarily for the treatment of advanced solid tumor bone metastases.

Six weeks later, the Center for Drug Evaluation (CDE) website indicated that Bliss Biopharmaceutical's first Antibody-Radionuclide Conjugate (ARC) drug, ¹⁷⁷Lu-BL-ARC001 injection, received implicit approval for its clinical trial application. It is intended for use in, but not limited to, patients with locally advanced or metastatic solid tumors who have failed standard treatment or for whom standard treatment is unavailable, marking the entry of an ADC company into the radiopharmaceutical arena.

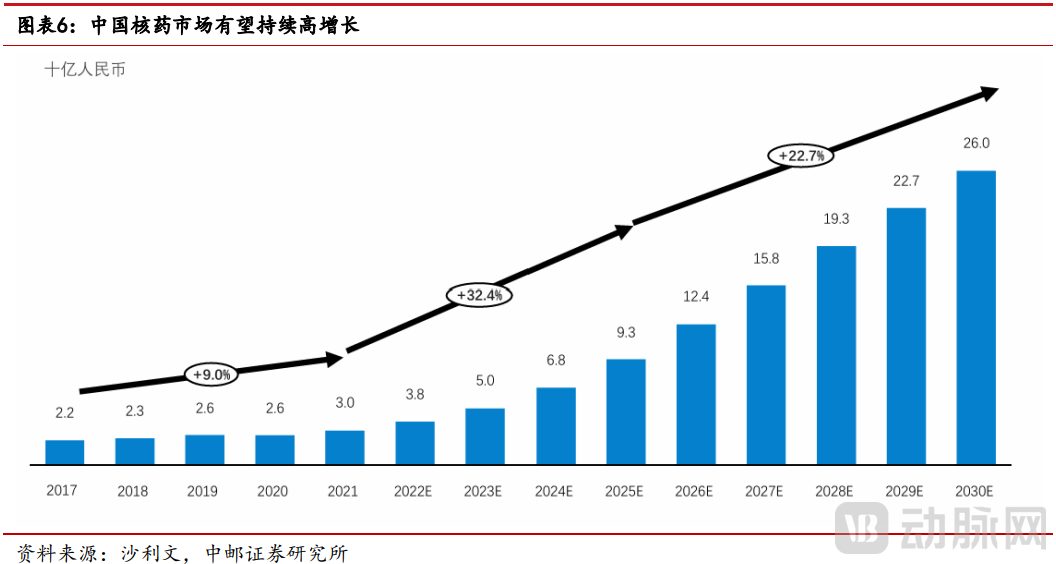

Data from Frost & Sullivan (which includes both diagnostic and therapeutic radiopharmaceuticals; the following discussion focuses only on therapeutic radiopharmaceuticals) indicates that China's radiopharmaceutical industry has entered a new phase of rapid growth, with a noticeably accelerated pace. Particularly, Radionuclide Drug Conjugates (RDCs) have now become the cutting-edge direction within the radiopharmaceutical field.

Figure 1. Growth Acceleration in the Nuclear Medicine Market (Source: China Post Securities)

Novartis currently holds a leading position in the field of radiopharmaceuticals. Beyond its two commercially available products, Lutathera and Pluvicto, the company has established a pipeline of multiple investigational candidates, including ¹⁷⁷Lu-NeoB and the next-generation radiopharmaceutical ²²⁵Ac-PSMA-617. The combination therapy involving ¹⁷⁷Lu-NeoB for breast cancer is currently in Phase I clinical trials, while ²²⁵Ac-PSMA-617, developed for prostate cancer, is also in global Phase I studies, though clinical trials in China have not yet been initiated. Both assets remain in early-stage development.

Outside of Novartis, other multinational corporations such as Bristol Myers Squibb, AstraZeneca, Eli Lilly, and Johnson & Johnson are actively entering the radiopharmaceutical domain, with a particular focus on the pioneering radionuclide drug conjugate sector.

In March 2024, AstraZeneca completed the acquisition of Fusion Pharmaceuticals, thereby gaining the FPI-2265 program—a potential new therapy for patients with metastatic castration-resistant prostate cancer. FPI-2265 is presently in Phase III clinical development and is expected to become the first actinium-based prostate-specific membrane antigen-targeting radioligand therapy available on the market.

In December 2023, Bristol Myers Squibb acquired RayzeBio for USD 4.1 billion, obtaining its platform for radionuclide drug conjugates and the core product RYZ101, which is intended for treating gastroenteropancreatic neuroendocrine tumors. Progress in the Phase III clinical trial for this product has been slow, primarily due to a shortage of actinium-225.

Through acquisitions, Eli Lilly secured two radiopharmaceutical programs, PNT2004 and PNT2001, which have currently reached the preclinical and Phase I clinical trial stages globally, respectively. Johnson & Johnson acquired Nanobiotix and gained the JNJ-6420 program, which is also at the Phase I clinical trial stage worldwide for prostate cancer treatment.

Chinese innovative pharmaceutical companies are also accelerating their development in the field of radionuclide drug conjugates. Grand Pharma is a front-runner in China's radiopharmaceutical industry and currently possesses ITM-11, a product targeting somatostatin receptors that is in Phase III clinical research.

New Radiomedicine Technology's NRT6003 injection is a yttrium-90 microsphere product for the treatment of liver cancer, currently undergoing Phase III clinical research in China. This therapy works by loading the radioactive isotope yttrium-90 onto carbon microspheres, which are then precisely delivered into the arteries supplying the tumor, enabling localized high-dose radiation to hepatocellular carcinoma lesions and thereby destroying the cancer cells.

Figure 2. Late-stage nuclear medicine projects (incomplete statistics by VCBeat)

In addition, emerging Chinese radiopharmaceutical companies such as Sinotau, Lanacheng Biotechnology, Yunhe Pharmaceuticals, SmartNuclide, Full-Life Technologies, Hexin Pharmaceuticals, and Bivision Pharmaceuticals have also begun entering the radiopharmaceutical field with early product layouts.

The sustained growth in radiopharmaceuticals is fundamentally driven by the critical role of radionuclides.

Guided by targeting vectors, radioactive isotopes are delivered directly to tumor sites to exert their therapeutic effects. Current research and development efforts by innovative biopharma companies are primarily focused on Lutetium-177.

As a therapeutic radionuclide, Lutetium-177 offers several key advantages:

·It has a relatively long half-life (6.7 days), which facilitates production, transportation, drug labeling, and quality control, thereby enhancing the accessibility of the therapy.

·During its decay process, Lutetium-177 also emits a small amount of gamma radiation. This enables SPECT imaging, allowing for the visualization of the radiopharmaceutical's distribution and metabolism within the body.

·The beta particles it emits have relatively low energy and a short average path length in tissue (approximately 670 µm). This results in a milder impact on bone marrow suppression while effectively irradiating the lesions, making it particularly suitable for treating small tumors and metastases. Furthermore, it minimizes damage to surrounding healthy tissues.

1) Lutetium-177 is an important prerequisite for the nuclear medicine boom.

Novartis's Lutathera and Pluvicto are representative radiopharmaceuticals utilizing lutetium-177 as the therapeutic radionuclide. These drugs are administered via injection into the patient. Through receptor-ligand targeting, they precisely bind to tumor cells—Lutathera targets somatostatin receptors, while Pluvicto targets prostate-specific membrane antigen. Once fixed at these target sites, the lutetium isotope emits beta particles that penetrate the tumor and surrounding cells, causing DNA damage and ultimately inducing cell death.

On January 19, 2024, at the ASCO-GI conference, Novartis presented updated Phase III clinical data from the NETTER-2 trial, evaluating Lutathera as a first-line treatment for gastroenteropancreatic neuroendocrine tumors. The study met its primary endpoint, demonstrating that median progression-free survival was extended from 8.5 months to 22.8 months—an increase of nearly threefold. The risk of disease progression or death was reduced by 72%, and the objective response rate reached 43%. Although Lutathera has shown significant clinical efficacy, neuroendocrine tumors are relatively rare. In contrast, the PSMA-targeting prostate cancer therapy Pluvicto has rapidly achieved blockbuster drug status.

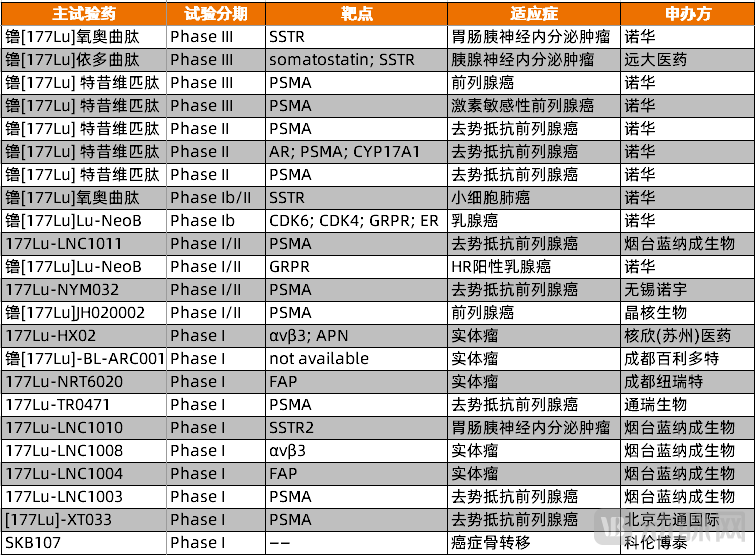

Chinese radiopharmaceutical companies are also actively developing therapies centered on lutetium-177. According to incomplete statistics, as of November 19, there are 17 innovative lutetium-177-based drug candidates in clinical stages in China.

Figure 3. Lutetium-177 innovative drug products currently advancing in clinical trials in China(Source: PharmaCube, VCBeat)

Lutetium-177 Edotreotide Injection, which has advanced into the clinical stage, was introduced by Grand Pharma in December 2021 through a licensing agreement with Germany's ITM. ITM-11 shares the same therapeutic focus as Novartis's Lutathera, both targeting patients with gastroenteropancreatic neuroendocrine tumors. At the 2025 European Neuroendocrine Tumor Society and European Society for Medical Oncology conferences, ITM presented the Phase III clinical trial results for ITM-11.

In this clinical trial, the primary endpoint of median progression-free survival was significantly longer in the ITM-11 group compared to the everolimus group. The overall study population showed an extension of nearly 10 months. Specifically, among patients with gastrointestinal-origin neuroendocrine tumors, median progression-free survival increased from 12.0 months to 23.9 months, while in patients with pancreatic neuroendocrine tumors, it extended from 14.7 months to 24.5 months. ITM-11 has already received orphan drug designation in both the United States and Europe, and its marketing application has been accepted for review in the U.S.

Meanwhile, ¹⁷⁷Lu-LNC1011 injection represents a domestically developed radiopharmaceutical product in China. Developed by Lanacheng Biotechnology, a subsidiary of Dongcheng Pharma, it is a targeted radioligand therapy directed at prostate-specific membrane antigen for the treatment of PSMA-positive metastatic castration-resistant prostate cancer, positioning it as a potential competitor to Novartis's blockbuster radiopharmaceutical Pluvicto.

¹⁷⁷Lu-LNC1011 utilizes PSMA targeting to concentrate lutetium-177 at tumor sites, enabling precise treatment. It is currently in Phase II clinical trials for adult patients with PSMA-positive metastatic castration-resistant prostate cancer. In the completed Phase I trial, preliminary efficacy was evaluated based on prostate-specific antigen response and radiographic assessments according to RECIST 1.1 criteria. Among six evaluable PSMA-positive metastatic castration-resistant prostate cancer patients, three achieved a reduction in PSA levels of more than 50% from baseline, resulting in a PSA50 response rate of 50%. These initial data suggest that ¹⁷⁷Lu-LNC1011 has the potential to become a PSMA-targeted therapy with enhanced efficacy.

2) The supply chain bottleneck for Lutetium-177 has been resolved.

While the R&D of radiopharmaceuticals continues to advance, breakthroughs in the supply chain have addressed key production bottlenecks.

Unlike traditional small-molecule chemical drugs or large-molecule biologics, radiopharmaceuticals involve the use of radionuclides, the production and application of which are strictly regulated.

Taking lutetium-177 as an example, reliance on imports has posed significant challenges. Not only must full payment be made months in advance, but supply sources are often unstable, creating considerable pressure on both supply chain security and corporate cash flow. More critically, lutetium-177 has a half-life of only 6.7 days, and shipping from other countries typically takes about four days to reach China. As a result, by the time manufacturers receive the material, nearly half of its radioactivity has already decayed, leaving an extremely narrow window for subsequent production, distribution, and clinical use.

The commercial availability of lutetium-177 has now been successfully addressed.

On June 25, 2025, the core product of Hefu-1, lutetium-177, was launched with an annual irradiation capacity exceeding 10,000 curies, sufficient to meet the demand across China. This marks a major breakthrough in China's ability to domestically produce medical isotopes. Hefu-1 is a medical isotope brand independently developed by the China National Nuclear Corporation (CNNC). The project utilizes the commercial heavy water reactor at the Qinshan Nuclear Power Base and has achieved large-scale production of lutetium-177 through three batches of irradiation and purification validation.

Currently, Qinshan Nuclear Power is collaborating with the Haiyan County government to develop the Haiyan Nuclear Technology Application (Isotope) Industrial Park, which will cover isotope preparation, radiopharmaceutical production, and supporting services. Novartis's radiopharmaceutical production project has also been established in Haiyan and is expected to commence operations by the end of 2026.

Meanwhile, Sichuan Haitong has successfully achieved lutetium-177 production utilizing the Jiajiang reactor. The company has already begun delivering its lutetium-177 products and plans to continuously expand production capacity, thereby boosting the development of the radiopharmaceutical industry in Sichuan.

These developments demonstrate that China has made significant progress across the entire industrial chain—from isotope production to radiopharmaceutical development—marking the onset of a phase of rapid growth for radiopharmaceuticals in the country.

Building upon the continuous expansion of research into the lutetium-177 radionuclide, scientific attention is increasingly shifting toward novel alpha-emitting radionuclides.

Compared to beta particles, alpha particles are larger and carry higher energy. This property enables them to break double-stranded DNA, causing severe cellular damage and destruction. Another critical advantage of alpha particles is their limited penetration range—typically only about 50 to 100 micrometers, which can be blocked by a mere sheet of paper. As a result, therapies utilizing alpha particles can achieve highly localized effects, effectively destroying tumor tissue while minimizing harm to nearby healthy cells.

In the field of alpha-particle therapeutics, innovative developments are primarily focused on actinium-225-based radiopharmaceuticals. Major multinational corporations have engaged in a series of acquisitions in this area, with Eli Lilly being the most active in recent transactions.

Figure 4. Layout of Major MNCs in Ac-225 Nuclear Medicine (Source: Ping An Securities)

In October 2023, Eli Lilly acquired Point Biopharma for USD 1.4 billion, gaining the pan-cancer FAP-α targeted program PNT2004 and the PSMA-targeted program PNT2001, both based on actinium-225. Throughout 2024, Lilly entered into successive collaborations with Aktis Oncology and Radionetics Oncology. In February 2025, the company further expanded its partnership with AdvanCell to jointly develop targeted alpha radionuclide therapies.

1) There are only two actinium-225 radiopharmaceuticals that have entered clinical trials in China.

Currently, the only clinical-stage asset in the field of actinium-225 among multinational corporations in China is Novartis's [²²⁵Ac]Ac-PSMA-617 (AAA817) injection. A combination therapy study related to AAA817 is advancing into Phase II/III clinical trials, while its monotherapy for prostate cancer has been submitted for clinical trial application in China.

Compared to Novartis's blockbuster drug Pluvicto, AAA817 replaces the radionuclide lutetium-177 with actinium-225 while retaining the same PSMA-617 targeting moiety. As a next-generation radionuclide drug conjugate in Novartis's pipeline, AAA817 leverages the alpha particles emitted by actinium-225 to induce more severe DNA damage in cancer cells while minimizing harm to normal tissues, showing potential for improved therapeutic outcomes.

A research team led by Professor Yue Chen from the Affiliated Hospital of Southwest Medical University has presented preliminary results in this direction in China. Among 11 patients, nine showed significant reductions in serum prostate-specific antigen levels after treatment, with six experiencing a decline of over 50%. The median progression-free survival was eight months, and overall survival was 12 months. Imaging-based responses indicated that seven patients achieved partial remission, two had stable disease, and two showed disease progression. These data suggest that ²²⁵Ac-PSMA is effective and well-tolerated in the treatment of advanced metastatic castration-resistant prostate cancer.

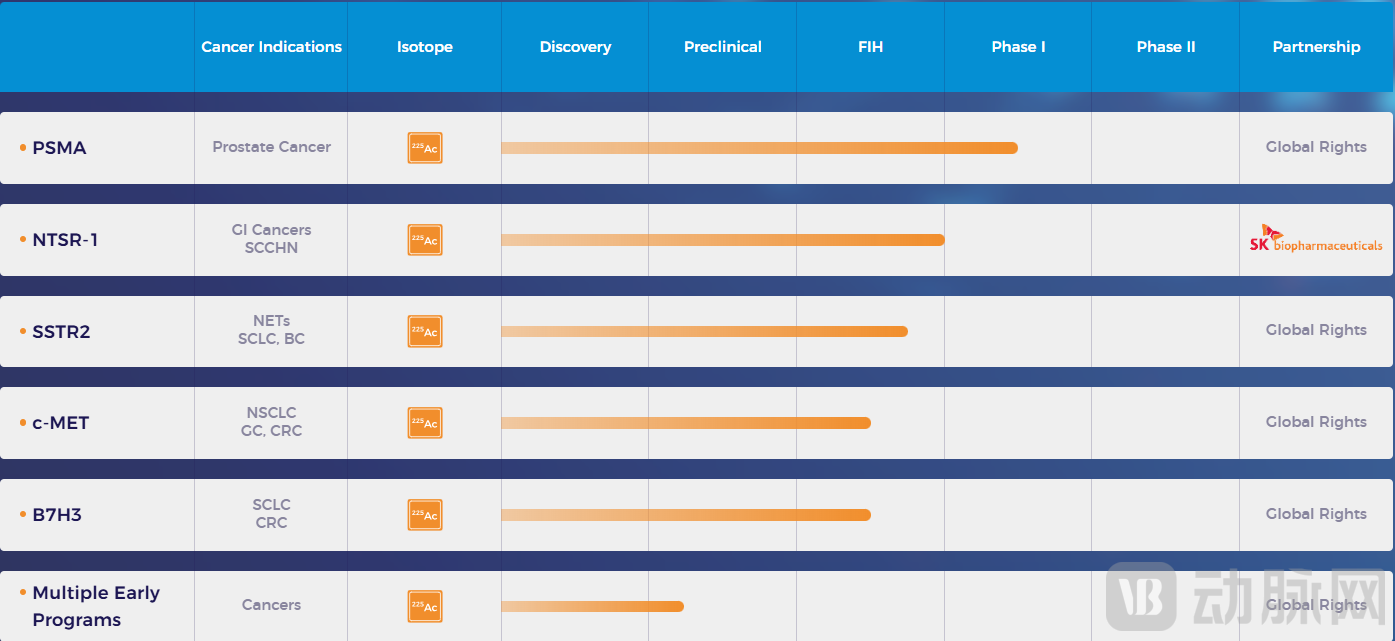

Among Chinese companies, Full-Life Technologies stands out as a leading player in the application of actinium-225. Its product, [²²⁵Ac]Ac-FL-020 injection, received implicit approval for clinical trials on November 10 and is intended for the treatment of metastatic castration-resistant prostate cancer. Another actinium-225 product from Full-Life Technologies, FL-091, was licensed to SK Biopharmaceuticals in July 2024. This product targets neurotensin receptor type 1-positive cancers, and the total value of the agreement reached USD 572 million, including an upfront payment and development and commercial milestone payments.

In addition to these two assets, Full-Life Technologies' pipeline includes multiple other actinium-225-based radiopharmaceuticals targeting markers such as SSTR2, c-MET, and B7H3.

Figure 5. Overview of Full-Life Technologies's R&D pipeline (Source: Company website)

In terms of products under development, only two actinium-225-based radiopharmaceuticals have entered clinical stages in China: Novartis's [²²⁵Ac]Ac-PSMA-617 and Full-Life Technologies' [²²⁵Ac]Ac-FL-020. This represents a significant gap compared to the number of lutetium-177-based radiopharmaceuticals in the clinical pipeline. The limited availability of the actinium-225 radionuclide itself is also a major constraining factor in radiopharmaceutical development.

2) The supply bottleneck of actinium-225 is much more severe than that of lutetium-177.

According to statistics, the current global annual production of actinium-225 is less than 10 curies, while the actual clinical demand has exceeded 1,000 curies per year, resulting in a supply-demand gap of approximately 100-fold. The supply bottleneck for actinium-225 is significantly more severe than that for lutetium-177.

The core reasons for this challenge lie in the complexity and high cost of production technology. Currently, actinium-225 for clinical use is primarily obtained through the thorium-229 decay chain (²²⁹Th → ²²⁵Ra → ²²⁵Ac), which not only offers limited yield but also involves an extremely intricate extraction process. Alternatively, producing ²²⁵Ac via electron accelerator methods requires using ²²⁶Ra as the target material, which exhibits strong radioactivity and high chemical toxicity, demanding stringent operational and safety measures.

Countries such as the United States, Russia, Germany, and Japan are actively researching technological pathways for actinium-225 production. In China, institutions like the Institute of Modern Physics, the Chinese Academy of Sciences and Tsinghua University have also achieved mass production of actinium-225, though it still falls significantly short of industrial-scale requirements. Moreover, the substantial upfront investment in production facilities and persistently high operational costs further constrain the large-scale manufacturing of actinium-225.

Previously, the radiopharmaceutical product RYZ101 from Bristol Myers Squibb had to pause its Phase III clinical trial due to a shortage of actinium-225. Whether viewed from the perspective of R&D or supply chain stability, actinium-225-based radiopharmaceuticals remain at an early stage of development.

Unlike conventional chemical or biological drugs, the radionuclide serves as the core component of a radiopharmaceutical and is key to its therapeutic effect. However, the supply of radionuclides is constrained, and therapeutic radionuclides have short half-lives—6.7 days for lutetium-177 and 9.92 days for actinium-225. To meet the demands of research and production, the radiopharmaceutical industry has developed a distinctly regionalized supply chain structure.

Leveraging the Qinshan Nuclear Power Base, Hefu-1 has officially launched lutetium-177, thereby driving the development of a full industrial chain in the Haiyan Industrial Park, encompassing radionuclide preparation, radiopharmaceutical production, and supporting services. Within this park, radionuclide products can be rapidly delivered to companies in need.

The Sichuan region also holds a significant position in China's radiopharmaceutical sector, hosting leading companies such as CNGT, Yunke Pharma, and Grand Pharma. Sichuan currently produces over half of the medical isotopes in China, providing a stable supply for downstream radiopharmaceutical R&D enterprises.

Furthermore, an integrated industry chain model is beginning to emerge. A case in point is New Radiomedicine Technology, which currently has four pipelines in clinical stages and has also achieved independent production and supply of more than ten critical radionuclides, including germanium-68 and actinium-225. Only by securing upstream radionuclide resources can radiopharmaceutical companies carry out R&D and production in an orderly manner. In this field, production, transportation, and administration are all a race against time, directly impacting final therapeutic outcomes.

Over the past few years, the radiopharmaceutical field has sustained significant attention. Even during periods of capital downturn, the sector has maintained strong interest. Supporters of this field are confident in its prospects due to the clear mechanism of action and substantial commercial value of radiopharmaceuticals. The current success of Novartis's Pluvicto has validated this perspective. Today, the entire industrial chain—from radionuclides to finished radiopharmaceuticals—is expanding rapidly, marking the sector's entry into a new phase of accelerated growth.