Hair loss giant Mandi files for HK IPO, backed by 57% market share and RMB 1.4B revenue

Recently, Mandi officially submitted a listing application to the Main Board of the HKEX. Structurally, this represents a carve-out by its controlling shareholder, 3SBio (HK01530). From an industry lens, however, it highlights a trend where niche leaders in the consumer healthcare sector are pursuing independent listings at an accelerating pace, as the capital market gradually recognizes and prices in the deep-seated value of their specialized focus, such as Mandi's in the anti-hair loss niche.

This shift is driven by a structural change in healthcare consumption trends over the past decade. According to a report (2024 Full-Channel Marketing Analysis of China's Healthcare Industry) by VZKOO, the health literacy rate among Chinese residents rose from 19.17% in 2019 to 29.70% in 2023, reflecting an expansion in health spending from reactive medication towards proactive management. Concurrently, data from CIC (China Insights Consultancy) shows that China's consumer healthcare market grew from RMB 931.3 billion in 2018 to RMB 1.8002 trillion in 2024, representing a CAGR of 9.9% over six years. Product systems tailored to specific scenarios and treatment courses are becoming a key component of corporate competitiveness.

Mandi is both a beneficiary and a driver of this transformation. Its success story is not merely about "going public on the back of a bestselling hair-loss treatment," but rather about maintaining a stable market position in the rapidly evolving hair health sector, which boasts a user base of over 300 million. This leadership is underpinned by its comprehensive strengths across products, channels, branding, and supply chain.

With its core business in hair health, Mandi is also expanding into dermatology and functional hair care. The company markets four main products across these areas, including OTC items, prescription drugs, and functional shampoos. Its product portfolio is centered around the flagship brand Mandi, a leading consumer healthcare brand for hair loss treatment in China. In dermatology, its product line includes Laizi® Tacrolimus Ointment.

Overview of Mandi Series Products (Source: Prospectus)

Consolidating Leadership in Hair Loss Treatment

In the hair loss drug market—characterized by mature active ingredients and a highly fragmented landscape—how did Mandi grow into a nationally dominant brand? Minoxidil is not a patented compound, and its technical barriers are considered relatively low. Yet Mandi has held the top market share position for ten consecutive years (claiming 57% of the total retail market and 71% of the minoxidil category in 2024). A first-mover advantage alone might sustain leadership for three to five years, but it cannot explain a decade of dominance. To understand that, one must trace the story back to its origins.

Mandi's origins can be traced back to a local pharmaceutical factory in the 1990s. At that time, China was witnessing a steady rise in hair loss cases, but the market lacked China-produced topical treatments that were both accessible and suitable for long-term adherence. Through market research in dermatology channels, the founding team recognized that hair loss was far from a niche issue, yet no Chinese brand was providing consistent and reliable treatment options. In 2001, the team launched China's first 5% minoxidil tincture, capturing the market with a product noted for its reliable supply, accessible pricing, and demonstrated efficacy. The company's subsequent acquisition by 3SBio provided greater R&D and commercial resources. As market demand for minoxidil-based products entered a growth cycle, Mandi steadily expanded its influence nationwide, thereby laying the foundation for its brand equity as it is known today.

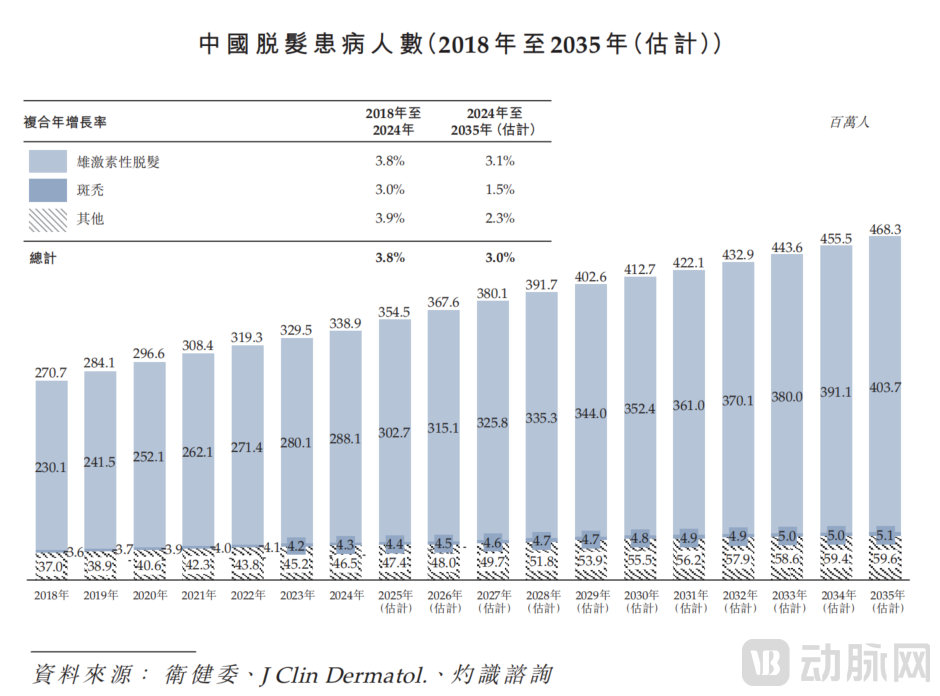

Number of People Suffering from Hair Loss in China (Source: Prospectus)

On the product front, Mandi has closely addressed real user pain points with nearly every iteration. In 2001, it launched a 5% minoxidil tincture, filling a critical market void. In 2018, the application of phosphate-buffered saline (PBS) formulation technology solved the industry-wide challenge of room-temperature storage stability. In 2024, it introduced China's first and only approved minoxidil foam. Utilizing a foam-based formulation for enhanced topical delivery, which improves efficacy and reduces skin irritation, the product saw first-year sales surpass 2.5 million units, generating over RMB 300 million in revenue. This launch also expanded the user base from diagnosed patients to younger demographics with sensitive or oily scalps and general appearance-conscious consumers, significantly broadening the brand's market penetration.

Beyond its core drug, Mandi is building a comprehensive treatment ecosystem. A new anti-hair loss shampoo with kopexil launched in 2025 sold over 500,000 bottles within six months. This creates a clear product pathway: tinctures and foam address the core issue of hair loss, shampoo improves the scalp environment, a professional customer service system provides usage guidance, and live-streaming content deepens user education. This integrated approach fosters high long-term repurchase rates. According to its prospectus, cumulative sales of Mandi's minoxidil products exceeded 50 million bottles from 2018 to 2024, underscoring the strong customer loyalty this ecosystem cultivates.

Channel strategy is another cornerstone of Mandi's brand strength. The company has built not just an omnichannel e-commerce presence, but a multi-tiered network covering both professional medical and mass consumer settings. Offline, its products are available in over 190,000 retail pharmacies and more than 2,000 medical institutions across China, with coverage exceeding 90% of the top 100 pharmacy chains. Online, it maintains a leading position in relevant OTC categories on platforms like Tmall and TikTok, while also tapping into the on-demand delivery segment through Meituan and Ele.me to enhance purchasing convenience. For consumer healthcare products, accessibility often outweighs price as a key conversion driver.

In summary, multiple, interconnected factors collectively forge Mandi's brand power in the hair loss drug market, making it a brand asset that transcends its minoxidil product origins.

Diversifying into Skin Health and Weight Management

Having consolidated its dominance in the hair loss sector, Mandi is now moving beyond reliance on a single product and expanding into two high-potential areas: skin health and weight management.

1Old Business: The "Cash Cow" Foundation Driven by Efficiency

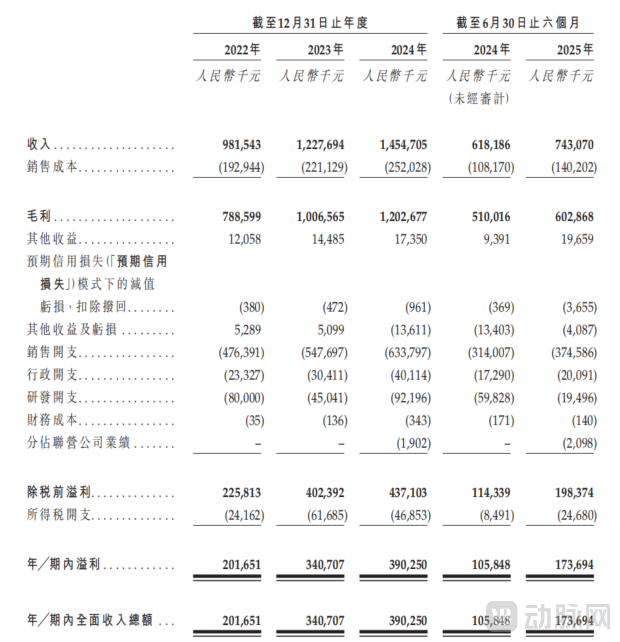

Financially, Mandi's hair health business has established a stable cash flow base. Between 2022 and 2024, the company's gross margin consistently maintained a level above 80%, recorded at 80.3%, 82.0%, and 82.7% respectively, while its net profit margin remained robust in the 20%-28% range. Sales efficiency is also notable; in 2024, it generated a revenue return of approximately RMB 2.29 for every RMB 1.00 spent on sales expenses. Meanwhile, its operating cash flow and net profit grew in sync for three consecutive years. These metrics indicate that Mandi's growth is driven by channel efficiency, brand recognition, and customer retention, rather than aggressive marketing expenditure, pointing to a high-quality growth model.

Mandi 2022-2025 (First Half) Consolidated Income Statement and Other Comprehensive Income

2New Growth: Dual-Track Layout Opens Up Billion-Dollar Space

While its established business remains stable, Mandi's strategic forays into skin health and weight management are paving the way for longer-term growth. Among these, Winlevi® cream and semaglutide injection (for weight management) represent its two most promising pipeline assets.

In dermatology, common acne is a highly prevalent condition with persistent demand. According to CIC, the patient population in China was estimated at approximately 121.2 million in 2024. Current mainstream treatments, largely based on anti-inflammatory and antibacterial agents, fail to address the root cause of abnormal sebum secretion, leading to issues with patient adherence and symptom recurrence. Winlevi® cream, which is in Phase III clinical trials in China, is a topical androgen receptor inhibitor that can influence sebum production by modulating the androgen signaling pathway. It is expected to submit a new drug application in 2027; if approved, it would represent a novel therapeutic option targeting sebum regulation in China. Alongside this, Mandi is advancing D2501, a candidate drug for vitiligo. Preclinical studies utilizing a novel transdermal delivery technology have shown superior efficacy in improving skin lesions compared to existing standard therapies. An application for clinical trials is anticipated in 2027, completing the company's innovative dermatology pipeline.

List of Approved Drugs for the Treatment of Common Acne Included in China's National Medical Insurance Drug Catalog

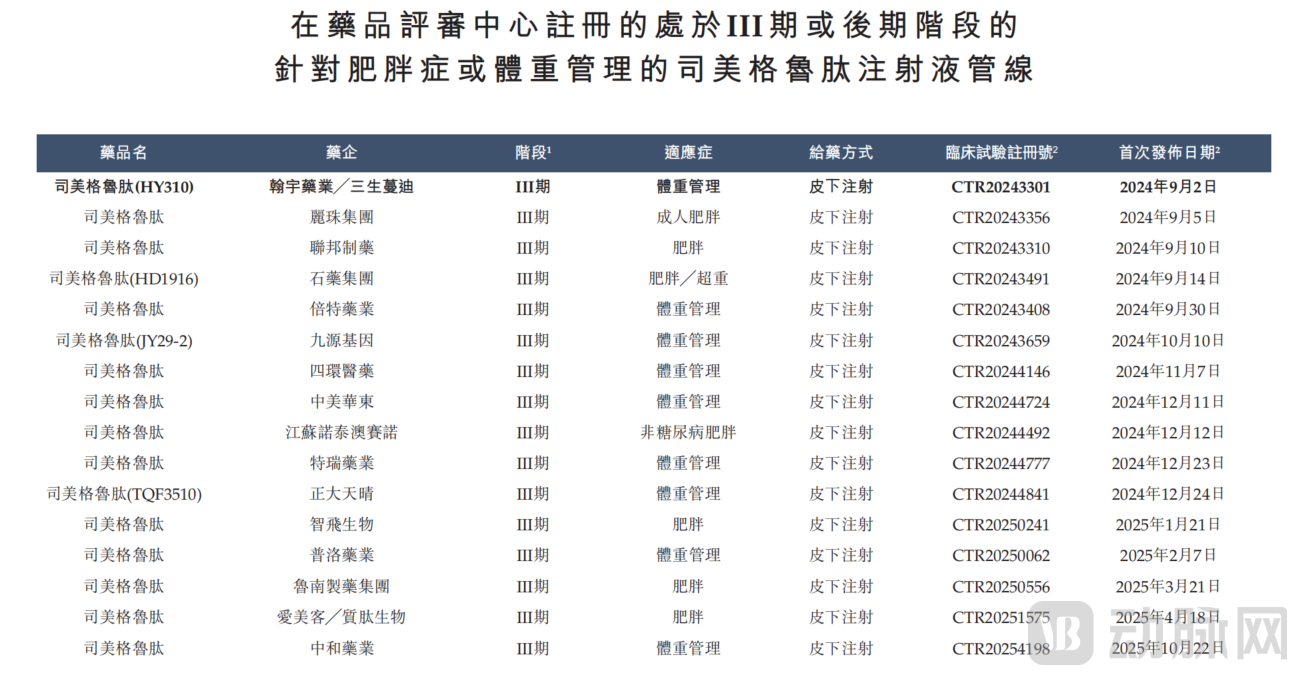

In the weight management sector, the semaglutide injection for weight management, being co-developed with Hybio Pharmaceutical, is currently in Phase III clinical trials in China. According to data, the number of obese patients in China is projected to increase from 277 million in 2024 to 342 million by 2035, with the corresponding drug market size growing from RMB 2.3 billion to RMB 80.4 billion, highlighting a strong and certain growth in demand. As GLP-1-based drugs gradually extend from prescription use to health management and lifestyle scenarios, brand operation capabilities and omnichannel reach will become key differentiating factors. The user operation expertise and distribution network accumulated by Mandi in the consumer healthcare sector will provide a differentiated advantage in the consumerization of such products.

Beyond this promising product, Mandi's weight management pipeline also includes the innovative multi-target drug candidate WS2505, which focuses on treating obesity and related metabolic syndromes and is currently progressing steadily through early-stage development.

Phase III and Later Stage Semaglutide Injection Registered with China's Center for Drug Evaluation (Pipeline List for Obesity/Weight Management Indications)

Overall, with a stable hair health business, innovative pipelines in dermatology and weight management, and strong commercial execution, Mandi is transforming from a single-product-driven brand into a multi-category, platform-oriented growth enterprise.

Investment Thesis and Inherent Risks

Capital markets value consumer healthcare companies based on three core dimensions: the stability of cash flow, the depth of the product pipeline, and the capability for category expansion. Mandi has established a relatively stable cash flow foundation from its hair health business. Coupled with multiple pipeline assets in dermatology and weight management, its long-term growth possesses clear anchor points.

However, it is important to note that behind the vast market potential and clear growth logic, Mandi's development still faces multiple underlying challenges. On the product front, the Mandi series contributes over 92% of total revenue. Should it face intensified market competition or policy adjustments like volume-based drug procurement in the future, the company's profitability could be significantly impacted in the short term.

The uncertainty of the R&D timeline is another concern not to be overlooked. In the first half of 2025, the company's R&D expenses fell to RMB 19 million, only one-third of the figure from the same period last year. Although the company attributed this decrease to reduced collaboration fees, the secondary market is highly sensitive to R&D spending in innovative drug companies. Fluctuations in investment could affect investor confidence. Furthermore, the clinical progress and regulatory approval efficiency of its two core pipeline assets—semaglutide and Winlevi®—will directly determine the timing of its second growth curve, making them key variables influencing the company's valuation.

The accelerating intensity of industry competition also tests Mandi's leading position. In the hair loss treatment sector, companies like Dafeixin and Conba Pharmaceutical are accelerating their market presence, continuously eroding market share. In the weight management arena, leading pharmaceutical firms such as Hengrui Pharma and Innovent Biologics are entering the GLP-1 drug development space, making market competition increasingly fierce. In the acne treatment field, pipelines from companies like Kintor Pharma are advancing steadily, potentially squeezing the market space for clascoterone cream. Going forward, Mandi must continuously maintain its dual advantages in formulation innovation and channel operation to consolidate its leadership amidst the intensifying competition.

In essence, Mandi has long transcended its identity as a mere hair loss drug company. Starting from hair health, it is building an integrated consumer healthcare platform that combines consumer brand operational capabilities with pharmaceutical R&D barriers. For investors, its core value lies not in its current scale of performance, but in its ability, over the next five years, to leverage the successful launch of its core pipeline assets and platform expansion to complete the transition from a niche leader to a comprehensive consumer healthcare platform.

Looking ahead, as Mandi continues to deepen its presence in hair health, skin care, and weight management, and steadily advances its core pipelines, its development path—characterized by "deep cultivation in core categories + expansion into potential sectors + external licensing for portfolio enhancement"—may provide a replicable growth model for the consumer healthcare industry. This will ultimately offer consumers more comprehensive, precise, and daily-needs-oriented health management solutions.