From catch-up to keep-up: how China's biopharma innovation is in sync with the global "Fierce 15"

China's pharmaceutical innovation capabilities are gaining global recognition.

Recent reports from top-tier international consulting firms McKinsey & Company and Boston Consulting Group (BCG) have, in a rare move, included China's pharmaceutical innovation in their discussions. Using multi-dimensional data, they substantiate the rise of Chinese innovative drugs across various fields and affirm the innovative caliber of China's pharmaceutical industry.

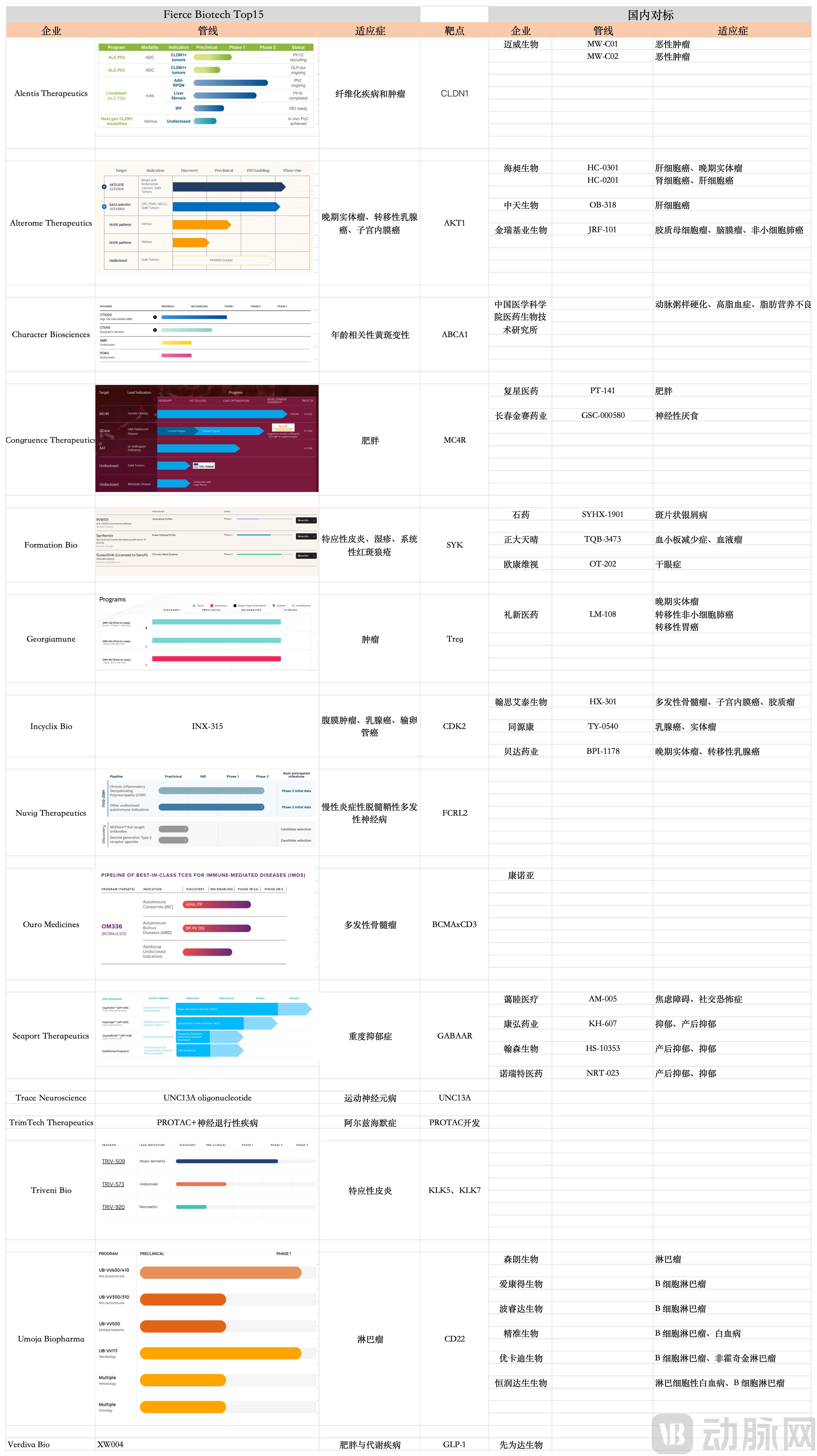

Furthermore, the annual "Fierce 15" list, published by the authoritative biotechnology media Fierce Biotech to identify the 15 most innovative and promising emerging companies in the biotech sector each year, is widely regarded as a barometer of industry innovation. Notably, in the 2025 list, when analyzed by target and indication, for most selected companies, there are domestic companies in China with comparable core pipelines, further highlighting the foresight of Chinese innovation.

Figure 1. China vs. Global: Head-to-Head Drug Pipeline Comparison by Target

Of course, competition within the same targets alone is not sufficient to fully illustrate the point. After all, the selected companies and their pipelines are all in relatively early stages, with none having a program in Phase 3 clinical trials, making it impossible to evaluate them based on clinical outcomes. However, a defining characteristic of this year's Fierce 15 is the significant emphasis placed on the development and construction of technology platforms. Among the 15 selected companies, 10 have built proprietary technology platforms, and at least 4 are extensively applying artificial intelligence (AI) within their platforms, aiming to use AI to accelerate drug discovery and development.

In other words, Fierce Biotech predicts that AI will be the most critical direction for pharmaceutical innovation in the coming years. Therefore, whether Chinese companies can match this level of technological advancement is a key indicator of their ability to keep pace with the Fierce Biotech innovation benchmark.

AI-assisted approaches will undoubtedly be a crucial path for future drug development.

Among the 2025 Fierce 15 companies, four specifically integrate AI into their drug discovery and development efforts: Alterome Therapeutics, Character Biosciences, Congruence Therapeutics and Formation Bio. Each company has developed a distinct strategic focus in applying AI technology. Below, we deconstruct several representative approaches to illustrate this diversity.

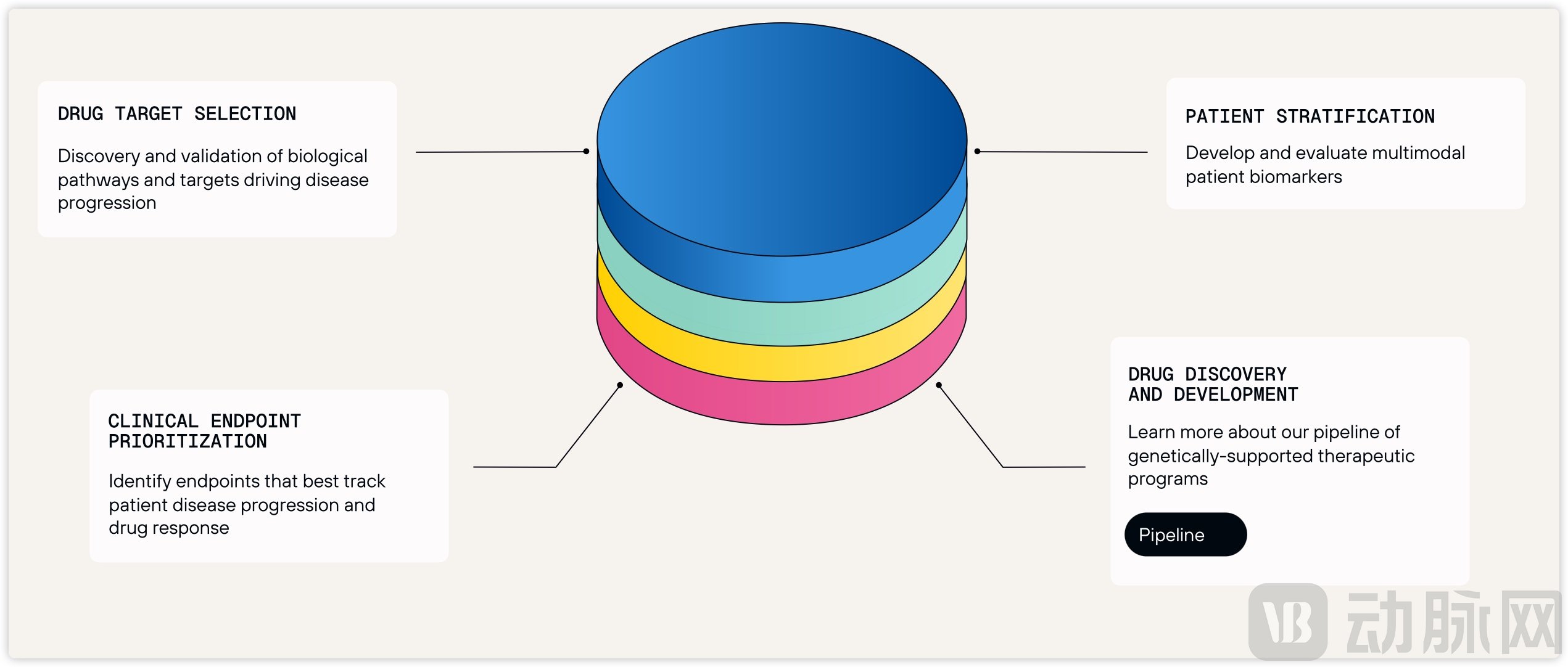

First is Character Biosciences, founded in 2019. Originally operating under a health insurance parent company, the biotech aimed to leverage vast insurance datasets to develop therapies for age-related chronic diseases. By integrating genomics, stem cell-derived cell models, and longitudinal clinical data, the company built an artificial intelligence-powered, genetics-driven drug discovery platform and set its sights on tackling age-related macular degeneration (AMD).

Currently, utilizing its AI platform, Character Biosciences has designed two lead candidate molecules: the lipid regulator CTX203 and the complement inhibitor CTX114. The company has also attracted the partnership of eye care giant Bausch + Lomb, with the two collaborating to develop new treatments for AMD. To date, Character has secured approximately $230 million in financing, with investors including Bausch + Lomb and Sanofi Ventures.

Figure 2. Character Bio's AI-Driven Drug Discovery Model.

Source: Character Bio Official Website

Character Bio's development strategy is grounded in the understanding that AMD is not a single disease, but rather a collection of disorders driven by distinct genetic factors—a key reason behind the high clinical failure rate of over 80% for new AMD therapeutics. The company has integrated patient genomics, imaging data, and clinical data from over 150 ophthalmic treatment centers across the United States to build a multi-omics database specifically for AMD. Using AI, Character Bio has classified AMD into at least five molecular subtypes with significantly different disease trajectories, thereby establishing a biological foundation for personalized treatment.

This deeply verticalized strategy has enabled Character Bio to accumulate rich, ophthalmology-specific data, develop proprietary algorithms, and build a significant technological moat. Building on its AI platform, the company has also begun researching molecular subtypes of other conditions, such as diabetic retinopathy and glaucoma. Looking forward, Character Bio aims to use AI to identify individuals with high genetic risk and intervene at early or even pre-disease stages across multiple therapeutic areas, with the ultimate goal of significantly preventing disease onset.

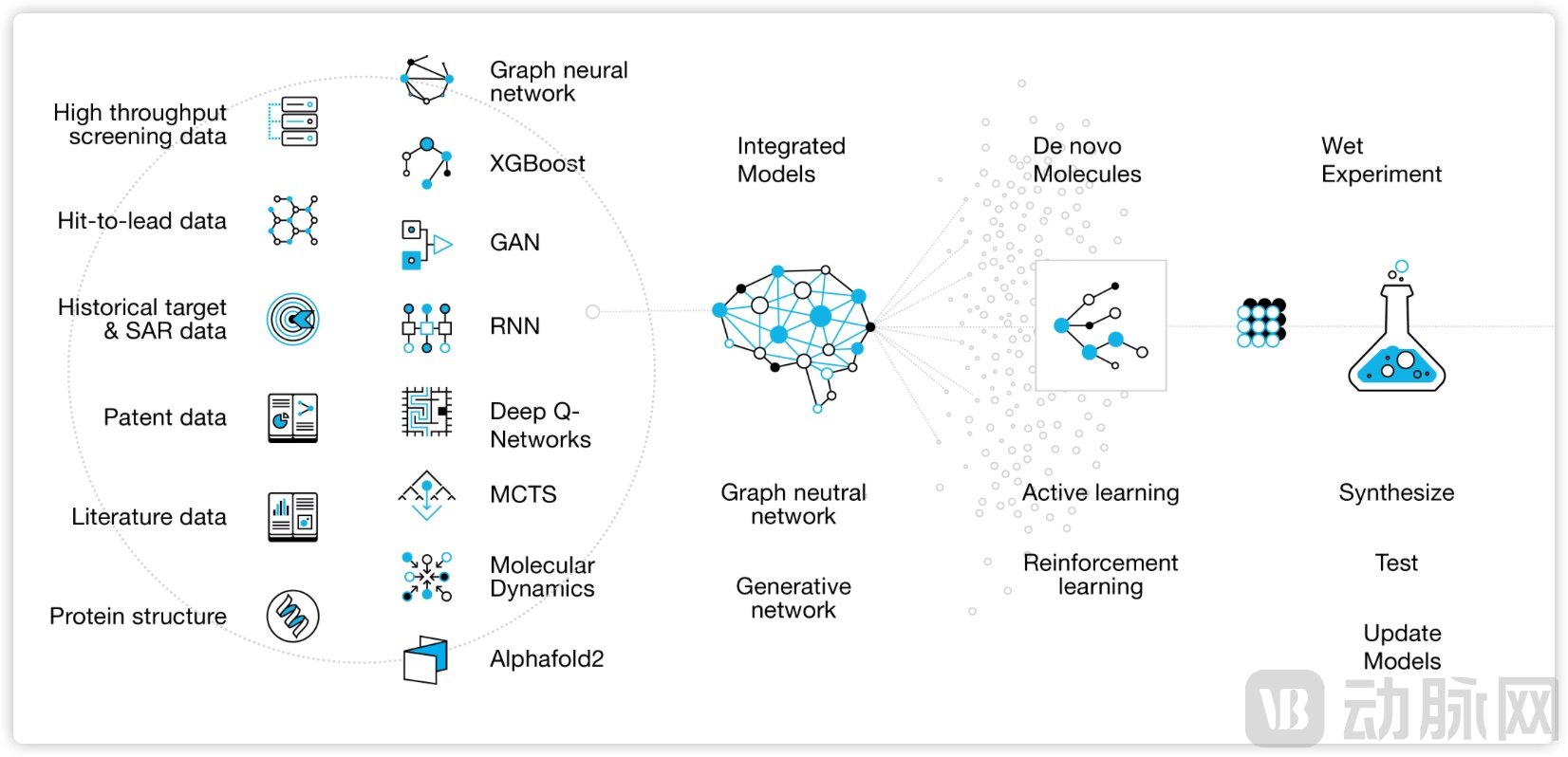

China is also home to several AI-driven drug discovery companies leveraging multi-omics data and genetic insights for disease subtyping and target identification. One example is Shanghai-based Drug Farm, founded in 2015, which similarly centers its approach on genetics and artificial intelligence to discover novel targets from the ground up and develop innovative therapies for hepatitis B, oncology, and autoimmune diseases. Its two core AI platforms—IDInVivo⁺, used to directly identify new drug targets in immunocompetent live animal models, and Medchem5, which employs multiple novel neural networks to optimize medicinal chemistry—accelerate the entire drug development process.

Figure 3. Drug Farm's MedChem5 AI Drug Design Platform.

Source: Drug Farm Official Website

To date, Drug Farm has discovered over 20 innovative drug targets. Its ALPK1 immune modulator, DF-006, has received approval for its Investigational New Drug (IND) application from the Center for Drug Evaluation (CDE) in China to initiate a Phase 1b clinical trial in patients with chronic hepatitis B (HBV). Another ALPK1 inhibitor, DF-003, had its peer-reviewed research published in Nature Communications. Furthermore, Drug Farm has entered into an agreement with Cincinnati Children's Hospital Medical Center (CCHMC) in the U.S. to explore DF-003 for treating cardiovascular diseases and hematologic tumors associated with clonal hematopoiesis. Concurrently, DF-003 has also received IND approval from the National Medical Products Administration (NMPA) of China to commence a Phase 1b trial in patients with the rare disease ROSAH syndrome.

Interestingly, comparing the development paths of these two companies reveals a kind of mirror-image symmetry. Character Bio starts from real-world human patient data, using AI to identify disease subtypes and processing multi-omics, heterogeneous data to translate clinical phenotypes into druggable targets. In contrast, Drug Farm begins with forward genetic screening in live animals, utilizing the PB transposon to create genome-wide random mutations in mice, rapidly converting genetically discovered targets into clinical candidate molecules.

Their similarities and differences are distinct. While both center on gene function and pursue First-in-Class targets, one focuses on correlation from human genetic variation, while the other focuses on causality from animal gene function. Both have built 'dry-wet' R&D loops and utilize AI to assist molecular design, yet one leans towards front-end target discovery, and the other towards back-end medicinal chemistry. Both emphasize high-quality data platforms and focus on diseases with clear mechanisms, yet one primarily utilizes human healthcare consumption data, while the other relies on experimental genetic data, leading to different therapeutic area emphases.

This analysis suggests their development paradigms are somewhat complementary. Character Bio addresses the 'last mile' from human data to medicine, whereas Drug Farm tackles the 'first mile' from mouse models to medicine. In the short term, Drug Farm's experimentally driven path may find easier traction within China's regulatory and reimbursement environment, as evidenced by DF-006's entry into clinical trials. In the long term, however, Character's data-driven model potentially has a higher ceiling. Should its AI-based subtyping gain clinical validation, it could fundamentally disrupt the treatment paradigm not only in ophthalmology but across chronic diseases.

Two other selected AI pharmaceutical companies also have Chinese competitors catching up.

Founded in 2021, Congruence Therapeutics has developed an AI-powered computational platform named Revenir, designed to characterize the specific biophysical defects of disease-causing misfolded proteins. The platform computationally designs compounds to correct these defects and rescue the function of the mutant proteins. Its key innovation lies not in simply inhibiting or activating a target, but in restoring the protein's normal function.

Congruence Therapeutics plans to submit a clinical trial application to Canadian regulators for its first candidate, CGX-926—a small molecule drug targeting genetic obesity—by the end of 2025. The company also plans to unveil two new pipeline candidates in 2026, targeting a variant of Parkinson's disease and alpha-1 antitrypsin deficiency. Furthermore, Congruence Therapeutics is collaborating with Ono Pharmaceutical in oncology and has secured investment from firms including OrbiMed and Investissement Québec.

In China, Moleculemind, a company focused on protein de novo design, leverages MoleculeOS—reportedly the industry's first fully functional AI platform for protein optimization and design—to advance AI protein technology from predicting existing structures to creating novel ones on demand. If successful, this technology could even be regarded as new infrastructure for the bioeconomy. Currently, Moleculemind has established collaborations with Cathay Biotech and Eli Lilly, and has received investment from HongShan, Baidu Ventures, and Lenovo Capital.

Additionally, China's Tianrang is dedicated to developing a deep learning platform for protein structure prediction. Its self-developed generative diffusion model for protein design, TRDiffusion, enables programmable de novo protein design, allowing for the "one-click generation" of proteins that meet specific descriptions. The Chinese ecosystem also includes several other companies applying AI to protein design, such as Synbio Technologies, Levinthal, Matwings Technology, Zelixir Biotech, Liying Biotechnology, and BioGeometry.

Another noteworthy company in the Fierce 15 is Formation Bio. It is not a typical biotech, as it doesn't even focus its core business on drug discovery. Instead, it aims to improve the most time-consuming and costly part of drug development: clinical trials. Originally named TrialSpark, Formation Bio built an integrated platform that connects the front-end (patient recruitment, e-consent) and back-end (data management, monitoring, and statistics) of clinical trials, eliminating manual steps to directly save time and budget for drug development.

TrialSpark demonstrated its value through successive collaborations with Novartis, Limbix, and Pfizer, and in 2021 secured a $156 million Series C round led by OpenAI co-founder Sam Altman, achieving a valuation exceeding $1 billion. Subsequently, TrialSpark ceased providing standalone clinical services to other companies and began acquiring external clinical-stage pipelines to advance rapidly using its own platform.

In 2023, TrialSpark rebranded as Formation Bio and, in 2024, completed a $372 million Series D round led by a16z with participation from Sanofi, Sequoia Capital, Thrive Capital, and others. Currently, Muse—an AI tool developed through the Sanofi-Formation Bio collaboration for optimizing clinical trial patient recruitment—is being used in Sanofi's Phase 3 clinical trial for multiple sclerosis.

China is also home to several similar companies. For instance, Deep Intelligent Pharma has built a vertical multi-agent AI architecture that covers the entire cycle from target discovery to clinical trial protocol design, data collection, auditing, analysis, and final reporting, achieving leaps in efficiency and accuracy within the clinical phase. The core logic of this model is not merely linear time-saving; it operates within a dynamic "hypothesis-action-learning-reflection" loop powered by a proprietary decision engine, learning from failed paths and adjusting strategies in real-time.

Furthermore, Chinese CRO players like WuXi AppTec are actively introducing AI and digital tools to optimize trial processes. Companies such as LinkDoc and Yiducloud have also accumulated experience in patient pre-screening and data management by building real-world data platforms, leveraging AI technology to enhance clinical research workflows.

It is noteworthy that AI-driven clinical trial optimization in China currently plays more of an efficiency-enhancing role. The disruptive aspect of Formation Bio lies in its "asset acquisition + AI value-add" business model, which moves beyond the traditional service-fee model for AI tools. In the future, Chinese AI-driven drug development companies should also explore more innovative business models, particularly those that move beyond service fees to create and capture value from assets, akin to Formation Bio's approach.

Overall, within the 2025 Fierce 15 list, AI-driven drug development companies are no longer appearing as mere technological accessories. Instead, they are achieving pathway-level innovations across the three core pillars of drug discovery, target mechanism research, and clinical development. This signals that AI in drug development is beginning to transition from a tool for empowerment to becoming the underlying operating system of the industry.

On the other hand, Chinese AI-driven drug development companies are transitioning from following benchmarks to running alongside global peers. In this process, they must also demonstrate the scalability of their platforms and the verifiability of their business models. Whether new models like Formation Bio's "AI-powered asset operation" can emerge in China will determine whether Chinese AI-driven drug innovation can ultimately redefine the industry's value chain.

China has risen from a follower in the global innovation landscape to a pivotal force.

In fact, the 2025 Fierce 15 list itself features tangible contributions from Chinese biopharmaceutical innovation. This year, the pipeline of the selected company Ouro Medicines originated from a license with China's Keymed Biosciences, while Verdiva Bio's pipeline was sourced from Sciwind.

In November 2024, Keymed Biosciences granted an exclusive license for the research, development, registration, manufacturing, and commercialization rights of its internally developed bispecific antibody, CM336, outside of Greater China to Ouro Medicines' subsidiary, Platina. This agreement earned Keymed a $16 million upfront payment, up to $610 million in potential milestone payments, and a minority equity stake in Ouro Medicines. CM336 is a BCMAxCD3 bispecific antibody currently in Phase 1/2 clinical studies and has received FDA Orphan Drug Designation for the treatment of Autoimmune Hemolytic Anemia (AIHA).

Similarly, Verdiva Bio's core pipeline also originates from China. Sciwind announced a global licensing and collaboration agreement with Verdiva Bio Limited for development and commercialization rights outside of Greater China and South Korea. The partnered assets include an oral GLP-1 receptor agonist and oral/injectable amylin receptor agonists, intended for use as monotherapies or in combination with GLP-1 receptor agonists. According to the agreement, Sciwind will receive nearly $70 million in upfront payments and is eligible for up to $2.4 billion in potential development, regulatory, and commercial milestones, plus royalties on future product sales.

Beyond the Fierce 15, recent reports from both Boston Consulting Group (BCG) and McKinsey & Company have praised the rise of China's innovative drug sector.

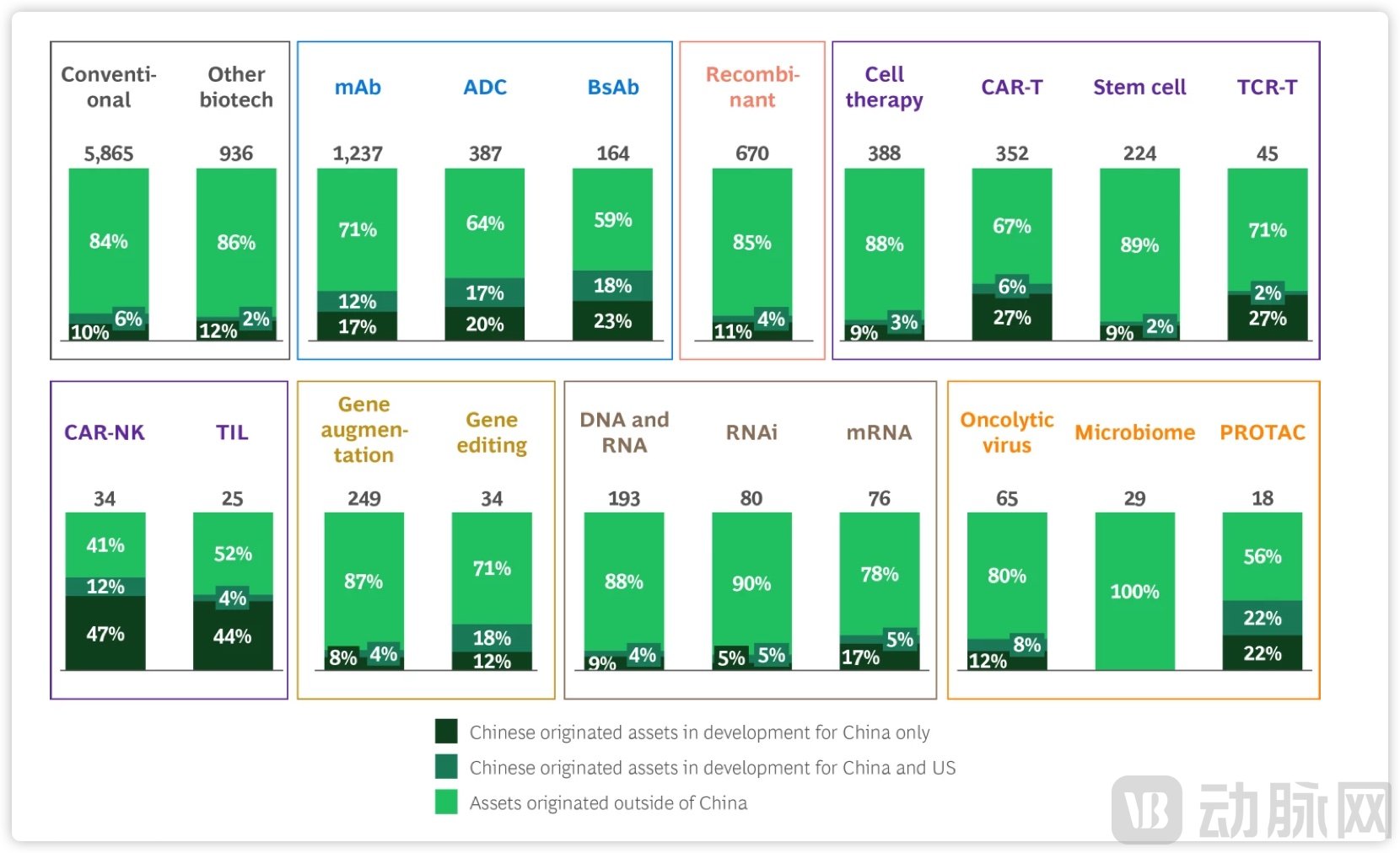

In its latest report, New Drug Modalities 2025, BCG tracks the development trends of six new therapeutic modalities—Antibodies, Proteins & Peptides, Cell Therapies, Gene Therapies, Nucleic Acid Therapies, and other emerging platforms. It attributes the global growth in new modality drugs to drivers like antibodies, GLP-1-based protein therapies, and nucleic acid therapies such as RNAi. Notably, the report incorporates the progress of Chinese companies for the first time, concluding that China is rapidly becoming a significant growth engine.

Figure 4. BCG's Assessment of China's Growing Role in New Drug Modalities.

Source: BCG, "New Drug Modalities 2025"

Specifically, Boston Consulting Group identifies China's innovation as having become the "second pole" in global new modality innovation. Firstly, China boasts over 4,000 active clinical-stage new modality projects, ranking second globally, only behind the United States. Secondly, more than 30% of global antibody and cell therapy pipelines now originate from China. Furthermore, nearly half of the Chinese R&D pipelines feature unique mechanisms of action with few global competitors. Finally, in 2025, 40% of business development deals conducted by the top 20 global pharmaceutical companies involved Chinese assets, demonstrating that Chinese innovation has gained significant recognition within the industry.

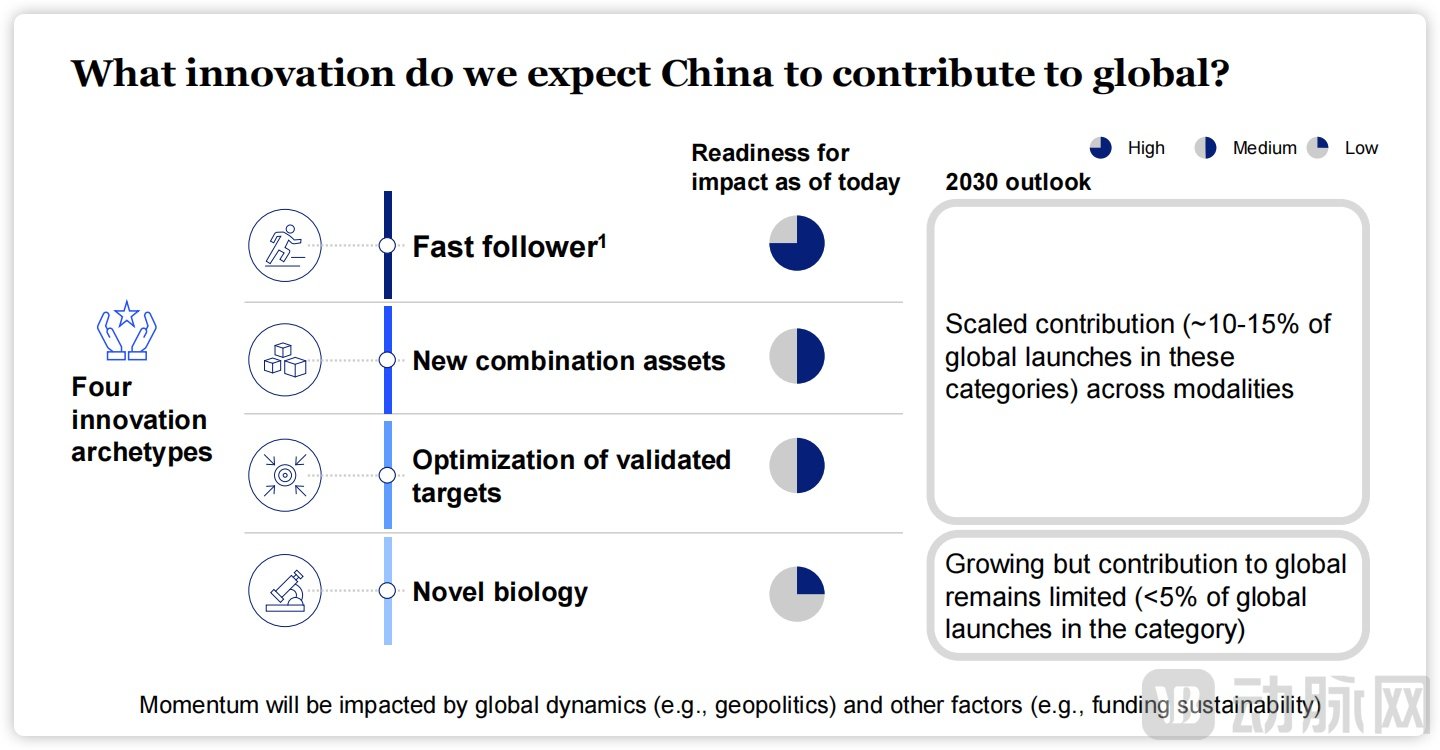

Similarly, McKinsey & Company's report, Building the bridge to global innovation, provides an in-depth analysis of Chinese pharmaceutical innovation and outlines its future development trajectory. The report is structured around three core chapters: the development trends of innovative drugs in China, China's unique development pathway, and the 2030 outlook for Chinese innovation.

Figure 5. McKinsey's Outlook on the Impact of China's Biopharma Innovation.

Source: McKinsey,"Building the bridge to global innovation"

Firstly, the report highlights a fundamental shift in China's standing within the global innovative drug industry, evidenced by the dramatic increase in its domestic pipeline—a 330% growth in oncology and a 512% surge in non-oncology assets in recent years. Secondly, it identifies that China's drug discovery phase is 2–3 times faster than the global average, achieving a 50%–70% compound acceleration, a trend that extends into the clinical development stage. This pursuit of R&D speed and cost efficiency is identified as a key driver behind the innovation explosion. Finally, McKinsey projects that by 2030, China will account for 10%–15% of all newly launched medicines globally.

Overall, 2025 marks a pivotal transition for China's innovative drug sector, moving from quantitative accumulation to qualitative improvement, with the industry evolving from being cost-driven to innovation-driven. By consistently increasing investment in basic research, refining institutional mechanisms that encourage original innovation, and exploring viable business model closures, China's innovative drug industry is poised to become deeply embedded within the global biopharmaceutical innovation chain and firmly secure this strategic niche.